Pre Approval vs Pre Qualification: What Homebuyers Need to Know

Many homebuyers use the terms pre approval and pre qualification interchangeably, but they are not the same. Understanding the difference affects how seriously sellers view your offer and how smoothly your purchase moves forward.

This guide explains what each one means, when each is appropriate, and why most buyers benefit from getting pre approved before writing an offer. If you are still early in the process, it also helps to understand what a mortgage broker actually does and how they fit into pre approval versus pre qualification.

Pre qualification is an estimate. Pre approval is a documented review that carries real weight with sellers.

What Is Mortgage Pre Qualification?

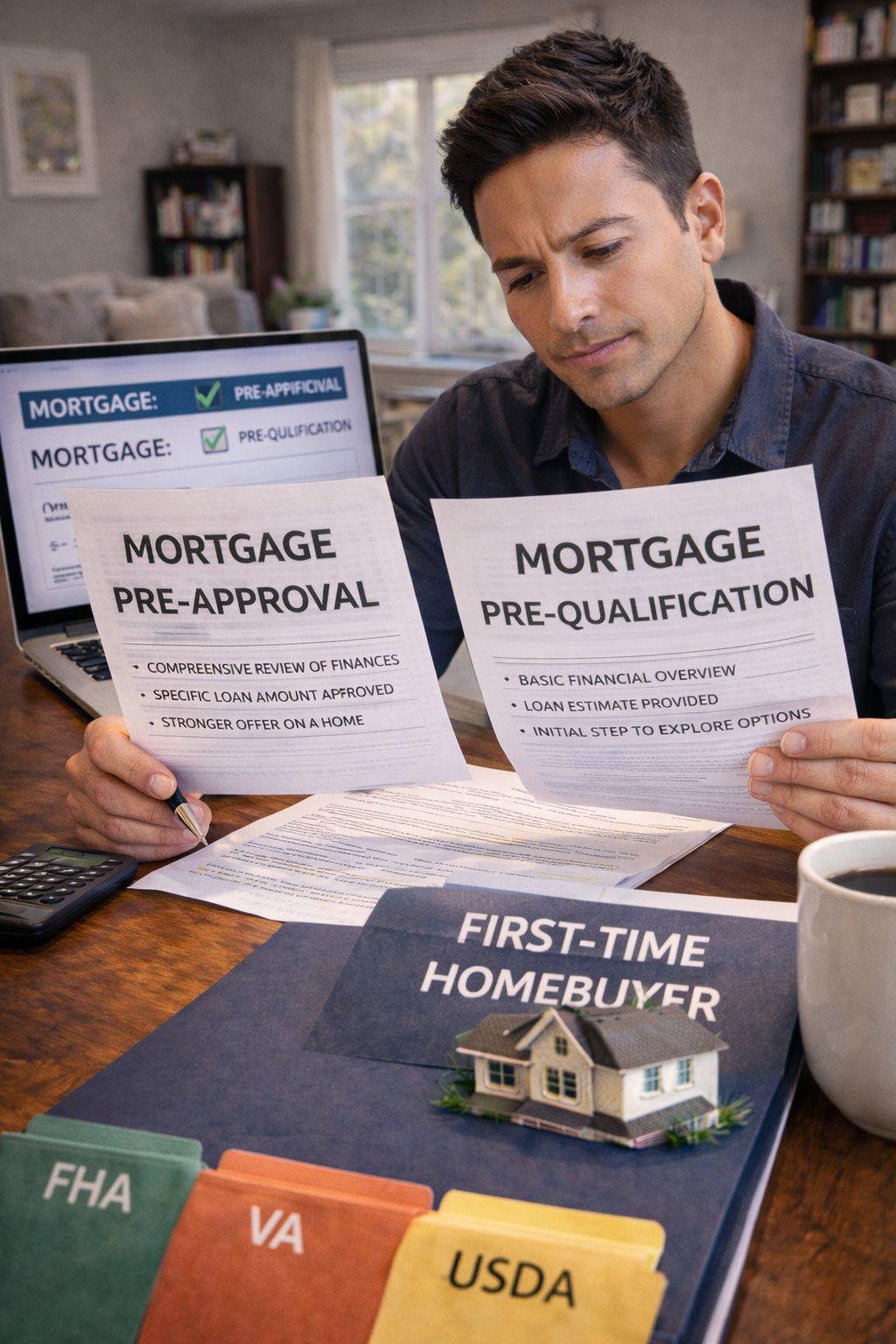

Pre qualification is a preliminary estimate of what you may be able to borrow based on information you provide. In many cases, no documentation is reviewed and credit may not be fully analyzed.

Typical characteristics of pre qualification

- Based on self reported income and assets

- May not include a full credit review

- No underwriting review

- Often generated quickly or online

Pre qualification can be useful early in the planning stage, but it does not provide the same level of confidence to sellers as a true pre approval. Many buyers mistakenly assume it is enough, which is one of several common mortgage myths.

What Is Mortgage Pre Approval?

Pre approval is a lender reviewed evaluation of your income, credit, and assets. It involves documentation review and a deeper analysis of your ability to qualify for specific loan programs.

What makes pre approval stronger

- Income and asset documents reviewed

- Credit report analyzed

- Program eligibility assessed

- Underwriting level review

For a deeper, step by step explanation of the process, see the full mortgage pre approval guide.

Pre Approval vs Pre Qualification: Key Differences

| Feature | Pre Qualification | Pre Approval |

|---|---|---|

| Document review | No or minimal | Yes |

| Credit analysis | Limited or none | Full review |

| Seller confidence | Low | High |

| Offer strength | Weak | Strong |

Which One Do You Need?

If you are casually exploring your budget, pre qualification may be enough. If you are touring homes, writing offers, or competing with other buyers, pre approval is the safer choice.

- Early research: Pre qualification

- Active home shopping: Pre approval

- Making an offer: Pre approval

Before choosing who to work with, it helps to know what to evaluate. Use this checklist of questions to ask a mortgage broker so you can compare options clearly.

Why This Difference Matters

In most real estate markets, sellers want confidence that financing will not delay or derail the transaction. A strong pre approval helps remove doubt and keeps deals moving.

- Compete against other buyers

- Avoid financing related delays

- Move toward closing with fewer surprises

If timing or expectations feel unclear, review how long it typically takes to close a mortgage and separate facts from assumptions by reading mortgage myths buyers still believe.

Pre Approval vs Pre Qualification FAQs

Does pre approval guarantee a loan?

No. Pre approval is not a commitment to lend. Final approval depends on the property, appraisal, and updated documentation.

Does pre qualification affect my credit?

Often no, but it depends on whether credit is reviewed. Pre approval typically involves a credit inquiry.

Next Steps

If you are serious about buying, the next step is a true pre approval so you can shop with confidence.

Related Mortgage Guides

This page is for educational purposes only and is not a commitment to lend.

NMLS: 80777

Licensed mortgage broker in Missouri, Kansas, and Louisiana.

Recent Comments